RL Blogs

By Market Analyst Dan

Aug 12, 2012A summary overview of refinery configurations in PADD 3 that can benefit from strategic debottlenecking. |

||||||||||||

|

No two refineries operate the same, and many variables contribute to the bottom line. Even the same exact refinery operated by two different owners can drive different value to the P/L statement.

I am not suggesting that these refineries are not profitable in today’s market environment. However, these refineries will find it challenging to compete in dynamic market environments over time. For petroleum refineries with a minimum capacity of 50 KBD crude throughput, I have selected the following sites:

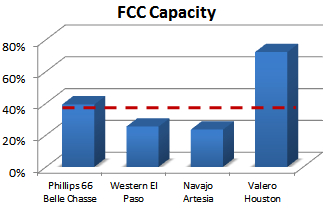

The chart below has a quick comparison of major refining units.

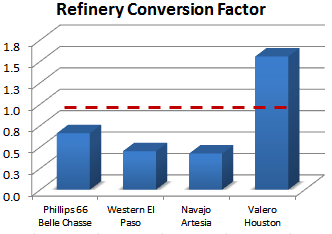

By normalizing refinery configuration based on conversion capacity, I have depicted the 4

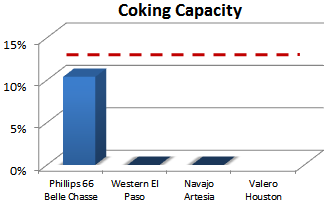

all have coking capacity lower than that of PADD 3 peers, with most of the refineries having very limiting resid upgrading capacity. Valero Houston does have some resid upgrading capability in a Solvent Deasphalting unit, but this type of configuration still comes with constraints.

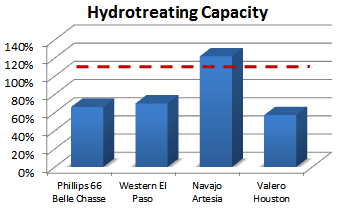

to find a refinery that feels comfortable with its hydrotreating capacity.

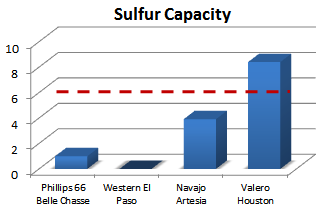

listed, El Paso refinery sulfur capabilities are also sub-standard.

The Valero sulfur capacity on a crude throughput normalized basis is high, but this is a bit misleading as that facility imports a significant amount of intermediates.

a refinery possesses hydrocracking or heavy hydrotreating capabilities. Also higher gasoline yields are not always favored.

In addition to the high level indicators of refining configuration discussed above, let’s dive a little deeper into some of the other details that support my views on these mismatched refinery units.

Western Refining - El Paso Cons

Pros

Navajo Artesia Cons

Pros

Valero Houston Cons

Pros

Phillips Belle Chasse

Cons

Pros

By stripping out all of the complexity related to supply chain logistics and location advantages, I have distilled refinery operations down to the simple common denominator of configuration capability. It is my belief that over time the most flexible refineries will always come out on top.

The refining business will always cycle with changing market drivers, and the ability to adapt operations will prove key. Refiners that struck profit in the past will not always have profits in the future. Assessing your refining capability relative to peers should remain a constant focus. | ||||||||||||

|

.png)

.png)

.png)

.png)

.png)