RL Blogs

By Market Analyst Dan

Jun 04, 2012The booming of North American crude oil production and dramatic shift in fuels (gasoline, jet, and diesel) are well published, but how do the themes connect? |

| Over the past year, the U.S. has seen a dramatic increase in crude oil production and refinery consumptions patterns. The United States and Canadian crude oil production has grown through technological enhancements such as hydraulic fracturing (“fracking”). Due to fracking, new pools of crude oil have been unlocked which previously were uneconomic to produce.

Fracking and synthetic crude upgrading have lead to massive increases of Canadian and U.S. Mid-Continent (PADD II) crude being offered in the market. Initially the logistical constraints for the Canadian and Mid-Continent crude limited its overall impact in the market. Recently, the market has reacted by building new and innovative methods for getting crude oil to key the market hubs of Chicago, Cushing (Seaway pipeline), and Houston.

New crude availability to U.S. refiners with access to the discounted crude has dramatically increased their competitive advantage. U.S. refineries have significantly increased their consumption of U.S. and Canadian crude oils. These crudes have declined in relative pricing from Latin American and African crudes by over $10 to $20/bbl, which translates to lower acquisition cost for U.S. refineries.

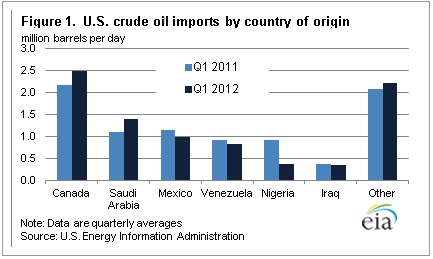

U.S. refiners have shifted over 16 million barrels per month of Nigerian (and other African crudes) crude to Canadian and U.S. crudes.

The other side of the increased crude production story has not been fully advertised by mainstream media. It’s the side of the “by product.” For years natural gas, which is often produced as a by-product of crude oil production, traded at a equivalent energy value (BTU equivalent) of 6 times under crude value.

This modest discount to crude did not overcome the difficulties of converting natural gas to electricity or fuel. The extra hurdles of transporting natural gas from producer to consumer often made the value proposition marginal. As fracking has increased the production of crude oil, natural gas production has increased as well. This has increased the discount for natural gas from 6 times to 33 times crude oil.

The ramifications of discounted natural gas are being felt all over the industry from the electrical generation business where coal fired plants are going out of business to U.S. trucking and rail industries converting upwards of 80% of their trucks to natural gas powered vehicles.

What does this mean for U.S. refiners? Its common knowledge that crude is the prime raw material for a refinery. Many people don’t realize that natural gas is the second most important raw material for a refinery because natural gas is used to fire heaters that heat crude oil.

Natural gas is also used as the raw material in the production of hydrogen. Without hydrogen, refineries cannot remove pollution impurities and refineries cannot hydrocrack heavy crude oil molecules to lighter more valuable fuels.

So the boom in Canadian and U.S. crude production through fracking and syncrude production has given the U.S. refineries a dramatic shift in their competitive capabilities. Their raw material cost have declined significantly over the past year.

In the mean time, competitors in Europe have seen their cost rise substantially without access to cheap crude and natural gas. Latin American refineries are struggling to merely remain operational. Asia refineries, often championed as the undoing of the U.S. refinery, are merely just trying to keep up with local demand.

The bottom line to all this is that the U.S. refiner can produce ULSD nearly at $2/bbl discount compared to a European refiner based on the difference in natural gas cost between the two markets.

When you compare the crude costs of Brent (Europe) crude and WTI (U.S.), Brent is currently $16/bbl over WTI. A U.S. refiner can produce diesel for $5/bbl less than a European refiner, assuming distillate yield is 30% of the overall crude feed to a refinery.

The cost of natural gas and crude oil allow the U.S. refiner to produce ULSD nearly $7/bbl less expensive than a European refiner. |

|