RL Blogs

By Steve Pagani

Aug 12, 2012Independent Refinery earnings in the second quarter 2012 were strong following similar themes from 2011 and 1Q201. But which refiners stood out from the pack? |

||||

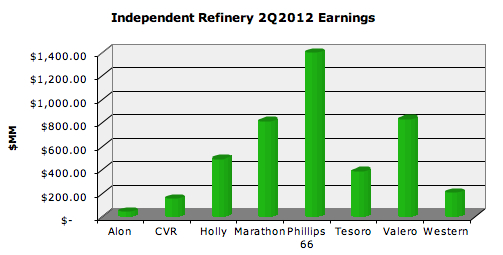

| We’re continuing our evaluation of the independent refiner’s financial performance for the second quarter of 2012 (2Q2012). Joining the independent refiner’s club is Phillips 66, which quickly jumps the front of the pack in terms of sheer size and earnings power.

Once again, we’re focusing on the independent refiner, because they often share very detail explanations of their earnings and operations. This allows us to better understand insights about actual earnings and industry trends.

The stories of the second quarter for the independent refinery earnings are quite simple, cheap crude and confidence. Most, if not all of the independent refineries capitalized on the Brent-WTI discount. More specifically, the independent refinery capitalized on discounted domestic crude versus foreign or offshore crude oil.

shareholder return or uncertain how to efficiently leverage their large stockpiles of cash?

All of the independent refiners had positive earnings in the second quarter, which is a significant improvement from the first quarter 2012. Let’s see who stood out from the pack.

Phillips 66

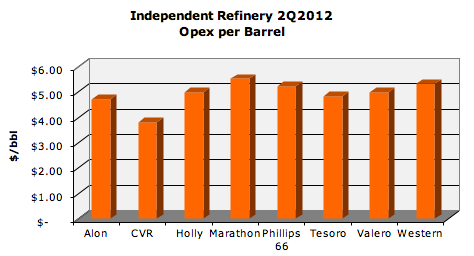

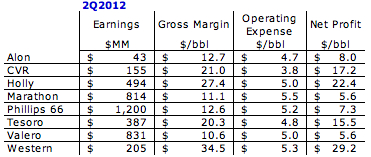

The new player to the independent refiner’s club, Phillips 66 beat all competitors with $1.2 Billion dollars in earnings. To some extent this should be expected due to their sheer size of operations compared to their competition. They completed the sale of the Trainer refinery to Delta which helped remove a poor performing asset from the balance sheet. The ding against Phillips may be that their overall net profit per barrel was among the lowest in the group at $7.3/bbl. This was a combination of highest in group operating expense and relatively low gross margin per barrel. This maybe the only downside of size where the overall benefit of PADD II refineries are diluted by the other refineries in the portfolio from a net profit per barrel standpoint.

Western, Holly, and CVR

All three refiners form the “best in class” group of independent refiners in terms of net profit per barrel for the second quarter 2012. These PADD II refiners all capitalized on inexpensive crude that priced at a discount to WTI. While inexpensive crude maybe the source of gross margin per barrel, each of these refiners also lead the pack in controlling operating expense. Especially Holly and CVR, which held operating expense at or below $5/bbl.

Western was negatively hit with product hedging losses in the first quarter 2012, but in the second quarter Western benefited from a $60 MM positive from product hedging. CVR’s earnings were directly attributable to very little turnaround cost (completed major turnaround in 1Q2012) and maximizing crude rates at Coffeyville refinery. CVR hit an all time high of 125MBD month average in June at Coffeyville. Holly also initiated a $127MM stock repurchase program along with $124MM in dividends payments.

Valero and Marathon

Valero and Marathon posted strong absolute earnings for the quarter posting $831 and $814, respectively. Marathon continued the trend of stock repurchase plans announcing a $850MM plan along with a plan to spin off their midstream assets to a MLP. Valero which previously spun off their midstream assets to a MLP continued the move by announcing the spin off their retail business to a MLP or third party. They also saw earnings increase as they realized the benefits of the acquisitions of Pembroke and Meraux refineries.

Tesoro and Alon Both refiners, Tesoro and Alon, lead the pack in keep operating expenses low at $4.8

inexpensive mid-continent crude relative to others in the group.

Summary The second quarter lead to strong results for all the independent refiners. The results of inexpensive raw materials (crude and natural gas) pushed the all refiners into the black for the year and further enhanced the cash positions for the pack leaders. Phillips 66 joined the club of independent refiners and their continued success will be a function of how well they can adjust to operating without of cover of Upstream.

| ||||

|

Related Blogs |

||||

|

|