RL Blogs

By Market Analyst Dan

Aug 04, 2013A summary overview of refinery configurations in PADD 5 that can benefit from strategic debottlenecking or outright closure. |

||||||||||||||

|

past. Most US refineries have enjoyed the benefit of the midcontinent crude disconnect. What may prove prudent at this very moment, is to determine if your refinery is worth putting on the sales block.

As they all say, buy low and sell high. The crude arb has tightened, so consider cashing out if you fall on this Dud list.

For PADD 5 petroleum refineries with a minimum capacity of 40 KBD crude throughput, I have selected the following sites:

As Tesoro Hawaii has been recently sold, I chose an honorable mention 5th refinery. Unlike the PADD 3 Dud refineries that served extremely niche markets, there appear to be surplus refining capacity with viable logistics to supply areas of the inefficient Dud PADD 5 refineries. This will increase likelihood of PADD 5 refinery closures over the next 8 years as RFS and LCFS requirements ramp up.

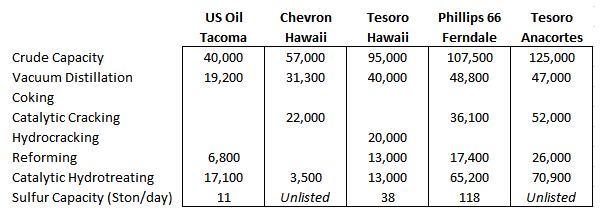

The chart below has a quick comparison of major refining units.

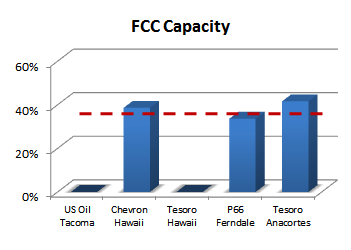

the Dud List fall outside of this band primarily due to the lack of gasoil and resid upgrading capabilities.

While PADD 5 does not carry the reputation of having refineries with large resid upgrading capabilities, there are many in the LA basin of PADD 5 that

comes with limitations. Tesoro Hawaii has a visbreaker, but that too is also inferior resid upgrading technology.

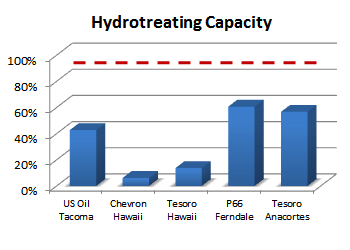

All of the PADD 5 refineries lack strength in conventional hydrotreating capacity. This was a common trend for the Dud refineries of PADD 3.

Hawaii refinery for example. Industry data shows that it does not have a naphtha, gasoline, or distillate hydrotreater.

The Tesoro Hawaii refinery is not that much further ahead with a lack of a gasoline and distillate hydrotreater. It is absolutely incredible to not have any real hydrotreating capacity in today’s environment. Essentially, this means that crude stocks processed at these two refineries are extremely sweet (i.e. low sulfur). This makes for very expensive feedstock costs.

To have competitive feedstock processing flexibility, refineries must meet the PADD 5 average of 85% hydrotreating capacity as a ratio of total refinery input. The most advanced refineries have 125% or higher.

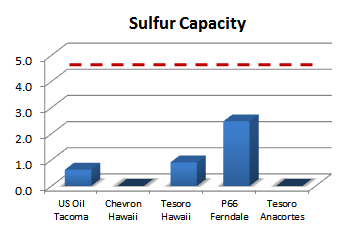

Similar to hydrotreating capacity, refinery sulfur capabilities provide indication on feedstock flexibility. For more mature refineries, you often

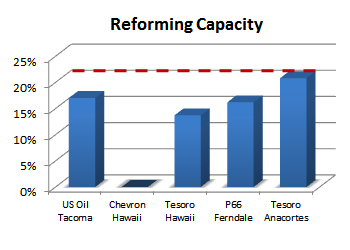

Reformer capacity provides indication in two areas: how well can a refinery maintain octane balance and how well can a refinery maintain hydrogen balance. Since PADD 5 lacks the concentration of 3rd party Hydrogen producers that PADD 3 enjoys, most PADD 5 refineries have to

becomes how do these refinery maintain octane balance? The Chevron Hawaii refinery shows no reformer capacity completely, so this suggests that most of the produced naphtha must be sold into export markets.

P66 Ferndale also shows lower reformer capacity than the PADD average. Using the rest of Ferndale’s configuration data (i.e. high distillate treater capacity, high Vac Capacity, and modest FCC/Alky), it would suggest that Ferndale manages crude diet to maintain octane balance as it has the ability to produce a higher amount of distillates and heavier products.

Tesoro Hawaii has a hydrogen plant, so that helps to offset H2 requirements. However, octane balances are strained with such limited reforming capacity. US Oil is such a small facility that it’s not worth discussing much. Interestingly enough, the PADD 5 Dud refineries mostly have adequate gasoil cracking capabilities when compared to the region peers. Three of the refineries meet or exceed the PADD average. Tesoro Hawaii does

In addition to the high level indicators of refining configuration discussed above, let’s dive a little deeper into some of the other details that support my views on these mismatched refinery units.

US Oil & Refining Co - Tacoma

Cons

Pros

Chevron Corporation – Hawaii Refinery

Cons

Pros

Tesoro Refinery – Hawaii

Cons

Pros

Phillips 66 Refinery - Ferndale

Cons

Pros

Tesoro Refinery - Anacortes

Cons

Pros

With the increasing pressures of the U.S. Renewable Fuels Standard (i.e. RFS2), it is inevitable that refineries within North America will shut down.

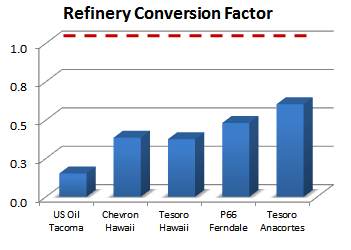

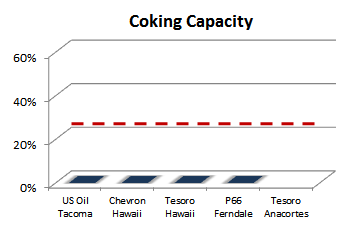

By stripping out all of the complexity related to supply chain logistics and location advantages, I have distilled refinery operations down to the simple common denominator of configuration capability. It is my belief that over time the most flexible refineries will always come out on top since market inefficiencies (i.e. midcon crude discounts) will self-correct.

The refining business will always cycle with changing market drivers, and the ability to adapt operations will prove key. Refiners that struck profit in the past will not always have profits in the future, so assessing your refining capability relative to peers should remain a constant focus area. | ||||||||||||||

|

|