RL Blogs

By Optimization Specialist Robert

Jun 20, 2016Understanding the fundamental market and quality drivers behind refinery gasoil pricing is key to maximizing value capture. |

||||||||||||||||||||||||||||||||||||||||||

| Often times a disconnect exists between your refinery trader and process engineer. Many traders do not understand how gasoil qualities affect process units, while many process engineers do not understand how market forces affect the price of gasoils.

Since commercial traders don’t like reading technical articles to improve their competencies, this article is meant to educate refinery engineers. Making process engineers more savvy in refinery economics proves to be a great way to leverage knowledge.

Let’s start with some basic concepts:

Understanding the disposition of gasoils in the market helps refiners extract the most value out of purchases or sales. To clarify my thoughts further, let’s assess each of the main points above.

Gasoil Market Disposition

It’s important to recognize one fact when trading gasoils: the most common use of gasoil is for FCC feed. This not only sets the base marker price of gasoil in parity to the 70/30, but it also decides the differential relative to the 70/30. The 70/30 is just a weighted average of the market prices of gasoline and diesel for a given region.

70/30 = 70% * (Price of Gasoline) + 30% * (Price of Diesel)

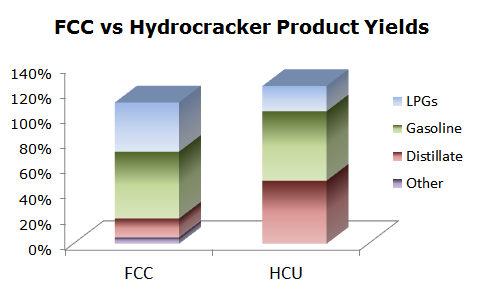

The 70/30 is a fair representation of FCC yields as roughly 50% of the product yield in a FCC is gasoline and 15% is distillate (LCO). Although FCCs also produce fuel gas, olefins, and bottoms, the 70/30 is a rough simplification since the value of lower priced products are offset by the volume expansion factor in the unit.

While the 70/30 is the base reference price, traders add premiums or discounts to the 70/30 based on other market factors. We call this the “differential” to the 70/30, and this ultimately decides the final trade price of a market gasoil. A couple of examples differential adjustments can be:

It’s important to understand the fundamental drivers of gasoil prices regardless of your intent in trading gasoils. Whether you have interest in purchasing gasoil as Hydrocracker feed, FCC feed, or for bunker blending, it’s important to understand what others are willing to pay for that gasoil. This will determine if you have any leverage or not.

the FCC, the relative price of gasoline to distillates will favor one buyer over the other. In a market where gasoline prices are significantly higher than diesel prices, the trader purchasing VGO as FCC feed will have a more favorable position compared to the trader purchasing gasoil as Hydrocracker feed. The converse will hold true when market gasoline and distillate prices invert.

Gasoil Qualities

Not all gasoils were created equally, so it’s absolutely critical to understand the quality of your gasoil regardless if you are buying or selling. The quality with the highest visibility is sulfur as there is a very liquid market for varying gasoil sulfur. Nominally speaking, the price difference between a High Sulfur VGO vs a Low Sulfur VGO is $3 /bbl.

While the price impact of sulfur on gasoils is fairly transparent, other qualities aren’t so much. Let’s take Aniline as the next example. Most FCC engineers know that aniline point can be a good surrogate of measuring FCC feed quality, but most traders do not know how to correlate trade price as a function of aniline measurement. Higher aniline will result in increased FCC conversion, and for my refinery I equate 10 deg Aniline change to $0.75 /bbl impact on FCC yields.

As one last example of understanding quality impacts, I’ll discuss carbon residue, or coke formation tendency. There are several different test methods to calculate carbon reside:

Different refiners may prefer different test methods, but essentially they all indicate the same thing. Since FCCs are heat balanced machines, feed carbon residue is extremely important to know when trading VGO stock. Most optimized FCCs operate at an air limit, so significant variations in feed carbon residue can result in significant operational changes, primarily feedrate reductions.

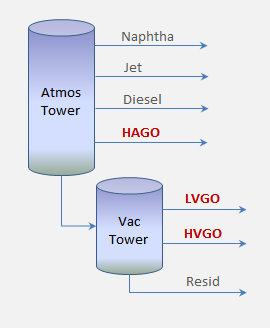

Traditional gasoils derived from HAGO, LVGO, or HVGO should have minimal carbon residue content, but some refiners slip atmospheric tower bottoms (ATB) into gasoil sales streams and contaminate the VGO. A distillation analysis of this stream may not reveal the true nature of the gasoil, but measuring CCR or MCR will be a saving grace. 1% variation on gasoil CCR can change gasoil pricing by $2 /bbl.

There are dozens of other impurities that can be measured, such as nitrogen, nickel, sodium, and vanadium, so just recognize that there are a lot of factors that can affect the price of market gasoils. The table below summarizes general ranges of qualities as well as rules of thumb on estimated price impacts.

Refinery Configuration

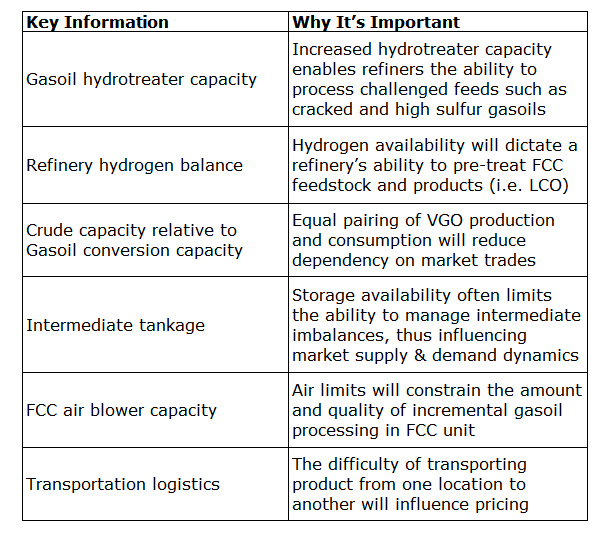

Leveraging refinery configuration is also an important factor when trading gasoils. The more you know about your own refinery configuration or a competitor’s can additionally improve your leverage. The following table can be a useful tool.

Supply & Demand

While all of the other factors discussed can have significant influence on the price of traded gasoils, the most important factor is always market fundamentals (i.e. Supply & Demand). In an ideal world where Supply and Demand are well balanced with high volume of trades, price variations will often follow factors such as qualities and transportation costs.

Unfortunately, refineries exist in all locations, and many do not have well balanced supply and demand. Some refineries produce more gasoil than can be consumed locally, while others have gasoil appetites higher than local supply. In steady-state operations the structural gaps can manifest in higher transportation costs, but in abnormal conditions this can really translate to significant discounts or premiums. Traders who have supplied refineries during Turnarounds or unplanned shutdowns know how much fun that can be!

As geopolitical, economic, and regulatory factors progress, gasoil supply and demand fundamentals have shifted. Some events have increased the demand of market gasoil, while other events have reduced the supply. An interesting academic exercise one can pursue is to track the price of VGO over the past 5 years. Key events to note include the following:

At the end of the day, the price of gasoils will vary quite significantly. They can trade at a discount of $10 /bbl to the 70/30 or they can trade at a premium of $10 /bbl. There are numerous factors that influence the price, and your job as an engineer, planner or trader is to maximize the value of your commodity. Regardless if you buy or sell, it’s important that you take into account all of the factors discussed above. | ||||||||||||||||||||||||||||||||||||||||||

|