RL Blogs

By Ralph Laurel

Sep 21, 2013With the changing parity of distillate prices, hydrocrackers have increased in popularity over the past 5 years. |

||||

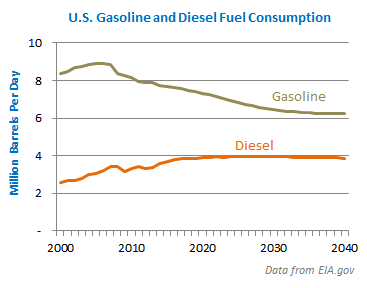

| Rewind time 20 years and every refining SME will tell you that they were a FCC expert. North American gasoline demand was high, and passenger vehicles were becoming bigger. A decade ago, developing countries (i.e. China) started to shift global demands towards the side of distillates.

maximizing distillate production instead of gasoline. Welcome to the standard that all other countries and the world has followed!

Aside from the declining importance of Cat Crackers to the U.S. refining sector, the increased focus on distillate product has changed how refiners now view their Hydrocrackers. What was once viewed as a high energy intensity and hydrogen consuming process, has now started to take the spotlight.

Before going much further in this discussion, let’s differentiate the two different types of hydrocrackers out there. I’m not talking about the ones with true 1st stage vs 2nd stage capabilities, but ones that differ in feedstock consumption. On one hand there are hydrocrackers that take primarily heavy distillate feeds (i.e. Light Cycle Oil), and then there are hydrocrackers that can take heavier feedstocks that range all the way to Light Vacuum Gasoils.

While both types of hydrocrackers have value, gasoil hydrocrackers are the ones that will shine in U.S. refining over the next 10 years. Distillate hydrocrackers had their 5 minutes of fame between 2006 - 2008 when ULSD specs hit North America. However, over the past 8 years, increasing catalytic capabilities of distillate hydrotreaters have reduced the length of LCO in the market, which have reduced the incentive to crack heavy distillates.

To understand the value of gasoil hydrocrackers, let’s first examine some general fundamentals:

Aside from equipment capabilities, two market factors influence the value of gasoil hydrocrackers in the refining industry. The first is the incremental cost of hydrogen. With the surplus of natural gas in North America following the fracking boom, it has become relatively cheap to produce hydrogen in recent past. In general, this has reduced the cost of operating hydrocrackers.

The second market factor influencing the value of gasoil hydrocrackers is the regional supply and demand balance of gasoils. As discussed in a prior article on FCC feed value, gasoils price relative to the marginal disposition of the commodity. In North America, the incremental disposition of gasoils is to a FCC unit. Since FCC’s produce a significantly higher amount of gasoline products relative to distillates, refiners who purchase gasoil to feed hydrocrackers have a significant price advantage when distillate prices fetch a premium relative to gasoline.

Hydrocrackers used to have unit margins of $10 /bbl a decade back, but it is not uncommon for many hydrocrackers to have margins in the $15 - $20 /bbl range today. In comparison, it’s unlikely for many FCC’s to have marginal economics beyond the $5 /bbl range.

With the shift in global macro-economics between fuel commodity prices and supply fundamentals, refiners today continue to increase focus on hydrocracker operations. While many factors support the value of hydrocrackers, let’s not forget the many downsides that include:

With all of that being said, the wild card factor that no one has connected to value the support of hydrocrackers is the implication of RFS. As refiners battle to maintain utilization over the next 10 years, every oil company will strive to place conventional product into the market that has been displaced by biofuels. Since jet fuel is exempt from RFS obligations, refiners who economically shift distillate production into jet (i.e. via Hydrocrackers) will have an advantage over others.

As every economic indicator points towards the long term sympathy of diesel prices, the stock of hydrocracker valuation should continue to climb. If you work for a downstream oil company in the U.S., I’m sure that there has been increasing focus on increasing distillate yield. The question to ask yourself is if enough has been done at your facilities?

| ||||

|

|