RL Blogs

By Ralph Laurel

Jan 19, 20142014 will be an extraordinary year for crude oil movement in the United States with over 2.5 MMBPD coming online. Hold on for the wild ride in the crude oil processing and pricing worlds. |

| U.S. pipeline landscape is set for another dramatic metamorphous in 2014. There will be an expected 2.5 million barrels per day (MMBPD) increased shipping capacity within PADD 2 and PADD 3.

The explosive growth in pipeline capacity has been years in the making as crude oil production in the PADD2 and PADD 3 areas, along with Canadian crude oil, has boomed to record levels.

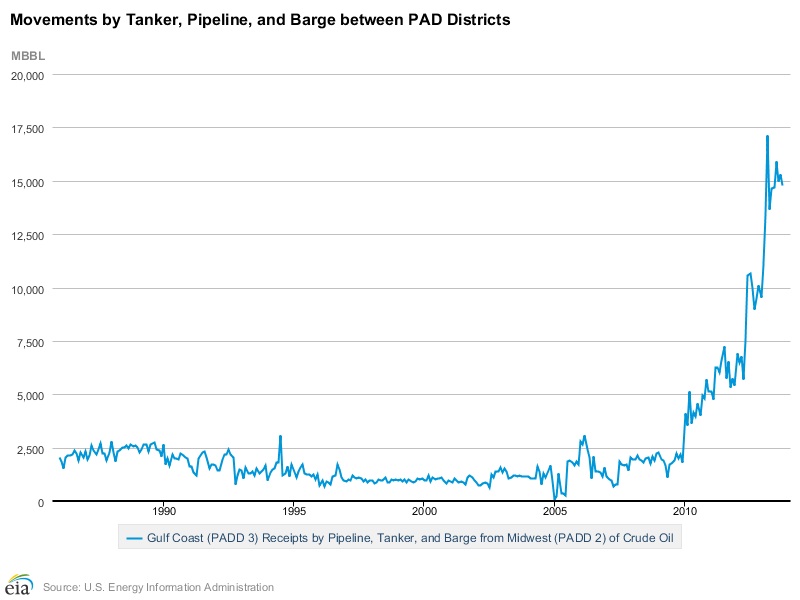

For the past 3 years industry analyst have watched excitedly as the WTI-Brent spread has expanded to record levels as crude oil flooded the WTI market center in Cushing, Oklahoma. As the WTI-Brent spread widened and sales discounts racked up, producers and midstream companies eyed ways to cash in on the opportunity to ship crude oil from production centers (PADD 2) to refining centers (PADD 3).

After several years of planning, permitting, and debate several key pipelines are set to expand or come online in 2014, which will allow for over 2 MMBPD of crude oil movement around PADD 2 and PADD 3.

We can categorize the new pipelines into three primary groups:

Moving Crude Oil from Cushing to Houston

Leading the way in the movement of crude oil from Cushing (PADD 2) to Houston (PADD 3) was the Seaway reversal. This has been in service for over a year and allowed up to 400 MBPD (thousand barrels per day). The second phase of the Seaway project is a new “twin” pipeline next to the original Seaway pipeline that will move up to 450 MBPD.

Many people know about the contentious and political debate regarding the Keystone XL pipeline that will connect Hardisty, Alberta, Canada, to Cushing, OK. Unfortunately, this pipeline project has been caught up in significant political and environmental debates.

Undeterred TransCanada has “quietly” continued the second phase of the Keystone XL project by completing the construction of their “Cushing Marketlink” pipeline which moves crude from Cushing (PADD 2) to Houston (PADD 3).

This new pipeline is completing line fill as of January 2014 and will soon begin shipping 700 MBD into PADD 3. Seaway and TransCanada projects are solutions to empty Cushing with over 1 MMBPD of increased take away capacity.

Moving crude from North Dakota/ Canada to Cushing

As Enbridge’s projects in Canada complete this project will allow increased crude oil shipments from Chicago to Cushing. The new pipeline capacity will be 60 MBD.

The Pony Express pipeline will ship crude oil from Guernsey to Cushing. North Dakota, Wyoming, and Colorado crude oil production continues to increase which necessitated the new pipeline from Guernsey to Cushing. Expected pipeline capacity will be at least 230 MBD.

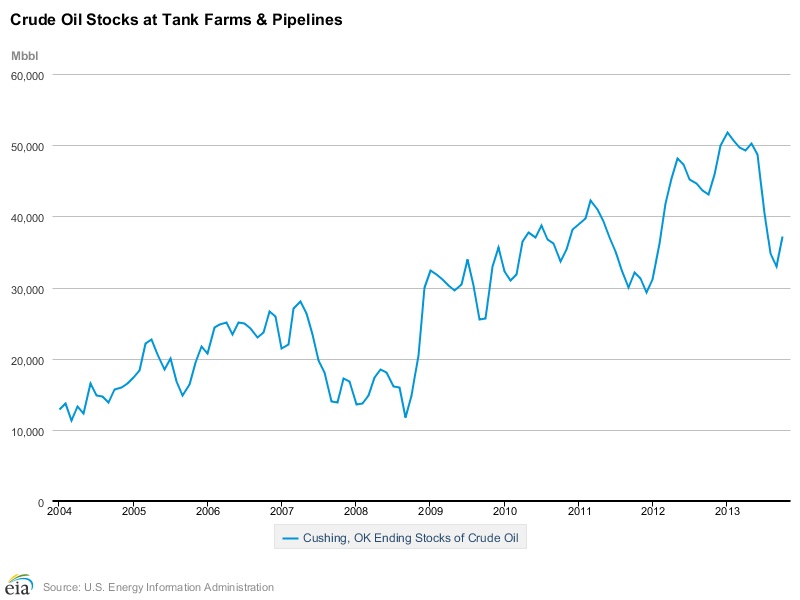

While Cushing crude oil inventory increased to 50 MMbbl supply from new growth in Bakken, Canada, and West Texas. The third segments of pipeline projects are pipelines to move West Texas Intermediate and West Texas Sour straight to Houston bypassing Cushing all together. Which effectively adds more take away capacity from Cushing.

BridgeTex pipeline from Colorado City to Houston will move 300 MBD bypassing Cushing. Magellan’s Crane pipeline is also set to expand capacity by 300 MBD to 575 MBD moving crude from the Permian basin to Houston.

While not falling into on of the three primary pipeline groups, equally important is the connection from Houston to New Orleans. Not to be left out the Mississippi River refineries in Louisiana will also get further connection to the Houston crude oil market by the expansion of the Shell Houston to Houma (“Ho-Ho”) pipeline by 50 MBD to 250 MBD.

As all these pipelines become operational expect to see dramatic shifts in the North American crude oil landscape. The flood of crude oil hitting PADD 3 will create further changes to the import crude oil landscape in PADD3 (and the U.S.).

Also, expect to see strengthening of the netback pricing for the producers in PADD 2 and Canada. It will be fascinating to see how refinery earnings change for the PADD 2 and PADD 3 refineries (especially the independent refineries) as pricing discounts reach equilibrium with incremental transportation and import parities.

One final observation should be that PADD 1 and PADD 5 refineries are essentially being left out of this pipeline party. Will their solution be further rail car supported supply chain? |

|

|