RL Blogs

By Steve Pagani

May 26, 2013Our independent refinery friends navigated through the traditional turnaround season in the first quarter of 2013 with relative success. Lets look and see how each refiner’s earnings turned out in the first quarter of 2013. |

||

| Independent refiners did much better in the first quarter 2013 (1Q13) compared to the same period of 2012. Each refiner earned more the first quarter 2013 compared to

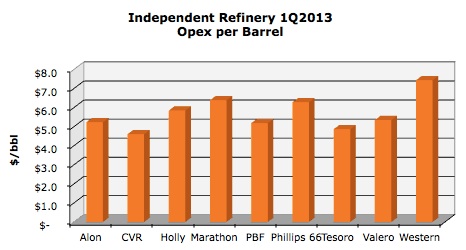

relatively stable opex charges allowed the refiners to be more profitable in 2013 despite a heavy turnaround season. Each quarter we highlight the winners and losers. In the first quarter 2013 the best independent refiners were CVR, P66, and Alon. This might seem like a strange grouping, but each had strong aspects of their operation that pushed them to the top of the independent refiners.

Leading the pack was P66 not because they are stellar performers from a low opex or high gross margin standpoint, but by pure volume. P66 is the big guy of the group processing over 2MMBPD. Even modest net profit per barrel combined with a lot of volume leads to high overall earnings. While they weren’t masters of opex or gross margin they were steady despite turnarounds so reliability and consistency paid off again; others across the industry could learn this concept.

CVR was near the top for gross margin per barrel for the independent refiners and combined with best in class opex made CVR one to the top independent refiners in the first quarter. While they also worked through turnarounds they increased overall crude processing in the quarter.

Alon didn’t earn the most or have the best per barrel metrics but they continued to right the ship compared to 2012. Alon had their best quarterly earnings in over a year. It’s clear that they are pushing more economic opportunity from the in-land crude discount by processing and utilizing logistical assets.

On the bottom of the independent refiner’s group were Tesoro and Marathon whom both suffered from extensive turnaround cost.

Several negative factors hampered Tesoro’s earnings in the first quarter; they worked through significant turnaround cost and low utilization. Tesoro’s primary footprint on the West Coast has limited their access to discounted inland crude, which limited their gross margin and limited their earning potential in a high turnaround quarter. They’ve made some sizable bets on rail economics so it will be interesting to see if they can improve their gross margin per barrel in the future.

Marathon was hit with significant opex cost as they worked through a high turnaround quarter. But they should be poised to capitalize on their new Detroit Heavy Oil Upgrader projects if the Canadian heavy oil discount remains. The Canadian heavy oil discount wasn’t their friend in the first quarter as WCS traded almost $20/bbl more expensive in the 1Q compared to previous months.

New guy PBF in the public independent refinery club came out with rather high opex per barrel. They also suffered from a pinch of railed Bakken economics. Of the group, they are probably the most at risk to the rail Bakken versus Brent economics. It will be interesting to see how they can leverage and optimize their extensive rail capabilities.

Western Refining was the classic example of high turnaround actively leading to high opex per barrel cost. Despite this, their access to discounted inland crude still propelled their gross margin per barrel. Bottom line is if you don’t process crude you can’t maximize the earnings on high gross margin per barrel crude oil.

Rounding out the middle of the pack were Valero and Holly, both worked through the typical first quarter turnaround activity but neither saw extensive increases in their operating expenses or declines in their earnings. I’d almost say that they were successful in the quarter. They didn’t create a massive hole to dig themselves out of for the rest of the year. | ||

|

|

.jpg)

.jpg)