RL Blogs

By Simon Jacques

Feb 02, 2015Analysis quantifying the costs and implications of the US Jones Act. |

||||||||||||||||||

| One Jones Act unit vs One Foreign Flag Vessel Unit

WHAT THE HERITAGE FOUNDATION GOT WRONG ABOUT THE JONES ACT

The Merchant Marine Act of 1920 (P.L. 66-261), also known as the Jones Act (JA) requires all vessels shipping cargo between two US locations to be US built, majority US-owned and at least 75% of the crew to be US citizens. There is indeed a conventional wisdom about the Jones Act (which is very located in the heart of the O&G industry saying that the Jones Act is a form of protectionism harming U.S refining margins.

U.S refiners have acknowledged that repealing the JA is nearly impossible, now the strategy is to push to get waivers on the Jones Act.

However waiving the Jones Act could add uncertainty in the U.S Shipping industry thus slowing capital investments in the U.S fleet with the unintended consequence of pushing-up rates higher.

One of the best-known and one most influential think tank, the Heritage Foundation, has written a piece entitled The Jones Act’s Costly Impact. The fact is that almost nobody including the Heritage Foundation, has ever provided substantive and solid benchmarking on the Jones Act.

One hint is that beyond this political debate, there’s always a complex market-driven process.

What is driving up the Jones ACT numbers?

The Economics.

Demand

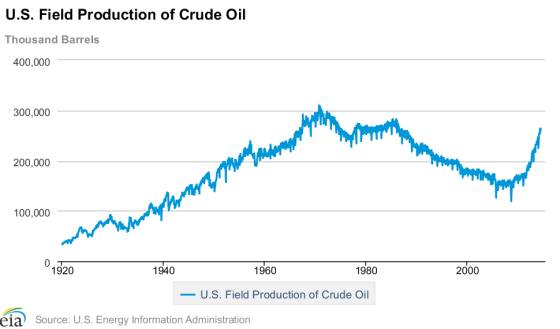

The U.S is producing Crude Oil at level unseen since 1986

Supply

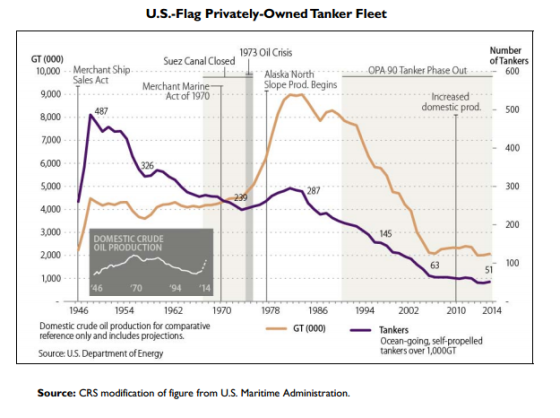

The U.S Flag Fleet tonnage is at an all-time Low

The market situation for Jones Act is (high demand/tight supply). Meanwhile the exact reverse prevails in the International Seaborne Freight Market (excess-capacity). The Jones ACT tanker market should not be regarded as different as any other markets; it’s the Supply and the demands that are moving charter rates up and down.

Oftentimes, a lot of folks talk about trade regulations but at the end it’s always policies within the economics context that drives up all those numbers in the real world.

During a recent panel discussion on oil exports, Graeme Burnett, senior VP for fuel optimization with Delta Air Lines estimated that oil shipping costs from the US Gulf Coast to Rotterdam would be $2/bbl versus $6/bbl from the Gulf Coast to Philadelphia.

To bring more clarity about the Jones Act Shipping Cost, we have decided to backtest the two following routes.

During October, USG/Europe was traded @ $12,558/day giving an estimate for this route @ $4.15/bbl. According to Burnett, the estimate for this route is $6/bbl.

We have backtested Burnett’s numbers and we only get $6/bbl if the vessel was chartered at $84,000/day at the top of the range.

Size does Matter

While The Marcus Hook Industrial Complex, PA can technically berth Suezmax and VLCC size vessels, the maximum draught on the Delaware River is 40 FT.

It means that a VLCC unit laden with North-Sea can’t be laden down to its load lines (full capacity) if the final destination is Trainer refinery and we can’t get 2$/bbl on a fully laden VLCC (70 FT).

(J) Simon Jacques (B) Burnett

On an Apple-to-Apple basis comparison, the conventional wisdom about the Jones Act can’t be proven. Freight costs/barrel estimates on the two routes aren’t significantly different.

Timing element

Timing of investment is a key to success in both U.S Flag and International shipping. This is because freight rates are sometimes very high for long enough periods of time to make a ship look more like a money machine than a normal production unit.

This timing element is within both Jones Act and FFV transportations costs. The estimate for the voyage was $4.25/bbl when Jones ACT rates were assessed in the $50,000/day.

Financial and Balance Sheet Matters

Because Jones Act is thinly trade it is difficult to draw the frontier between operational and capital costs on a balance sheet thus getting a precise $/bbl estimate per voyage.

Because Jones Act charters signed between parties have very long terms, they are susceptible to be capitalized by an accountant pen at an Oil Refiner. If the charter is capitalized, the charter liability will be treated as an asset on the balance sheet.

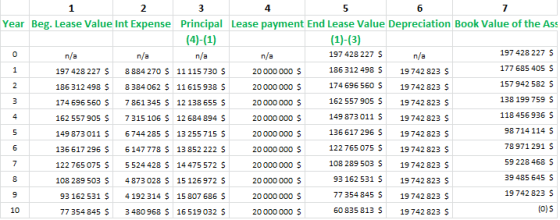

3.48$ is the implied transportation cost/bbl for a Jones ACT MR-Size Tanker under these assumptions:

The asset value of this charter will be determined at the delivery of the vessel. PV Charter = Sum Monthly Rate/ (1+i)n

Example:

Using the straight-line depreciation = $19,742,822.73 /year

We can add the voyages expenses per month to the capitalized lease cost per barrel to obtain a total cost per barrel.

(Capitalized lease cost ($/per bbl/Month) + Voyage expenses $/Month) / barrels. We get $3.48/bbl

The Suezmax Case

So far we have compared the 45,800 DWT M/T Pennsylvania with a FFV unit of a similar size.

Now we would like to compare a bigger size: the Suezmax (150,000 DWT).

Cost JA Suezmax $/bbl 1.28* $/bbl 2.11** $/bbl 4.22***

*2 RV/month on a JA newbuilt Suezmax 10 years charter= $1.28/bbl (assuming API 40, 991,000 bbls cargo, 15/13kts, 6d laden, 6 days ballast, 2 days loading, 1 day disch., +5% sea/weather margin)

**1 RV/month on a JA newbuilt Suezmax 10 years charter= $2.11/bbl (assuming API 40, 991,000 bbls cargo, 15/13kts, 6d laden, 6 days ballast, 2 days loading, 1 day disch., +5% sea/weather margin)

***.5 RV/monthon a JA newbuilt Suezmax 10 years charter=$4.22/bbl (1 RV/2 months , (because of unfavorable oil markets conditions or because the unit is used for storage).

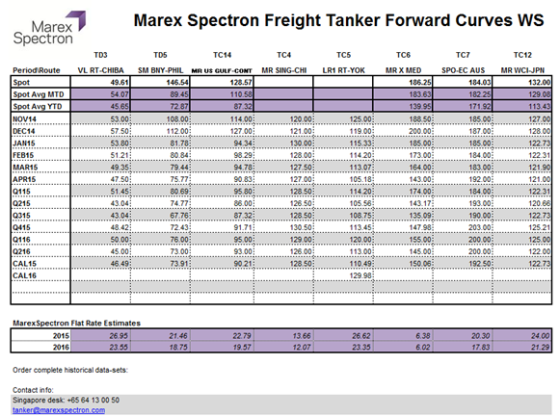

FFV Suezmax TD5 Bonny - USEC

TD5 is the Baltic assessment for the Suezmax route TD5, 130,000 mt W Africa to US Atlantic coast, 130,000 mt.

As you can see the Suezmax market is red-hot right now, we are well-above the 2$/bbl assumed by Burnett. The Suezmax markets have climbed to their highest levels in over six years.

****Marex Spectron Tanker curve spreadsheet 2014-11-19 , we have used their $/MT with a API for bonny @ 35.3 degree to get $/bbl.

Jones Act Tanker, TTT (trader trading tool)

Shipping markets are recognized today as a key component of commodity trading. For those actors who own vessels readily available for various destinations, “geographical arbitrage” may be achieved when the IFS is > than Cost shipping.

The Jones Act tanker unit in the spot voyage basis USGC/USEC is traded ≤ the marginal light crude oil price differential between the USEC and the Gulf Coast. This Implied Freight spread is tying up cash prices between the U.S Atlantic Coast and the U.S Gulf cost.

We have also demonstrated that spot rate are persistently priced above the long-term implied $/bbl. The $5 to $6 cost/bbl from Houston to USEC in the spot market reflects;

A certain convenience yield or benefit of owning a unit for a voyage in the spot market?

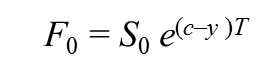

No-Arbitrages Cash and Carry Formula. [1.1]

$2.11 = $5 e (0.045–y )10

Solving y: 2.11=5e( 0.045-y)10 ln(2.11/5)=( 0.045-y)*10 ln(2.11/5)=( 0.45 -10y) [ln(2.11/5)-0.45]/10 = y y= 0.13127

The high convenience yield, could be explained by the relative scarcity of the Jones Act fleet ((current utilization for the coastal fleet is in the 90% to 95% range and the listing is limited.

Finding the theoretical forward value by interpolation.

F0= Soe(c-y)t [1.1] So= $6 $2.11 = 6e(0.045–0.13127)*10 $2.11< 2.53213

It suggests selling spot voyages and buying a long forward position on Jones Act.

Brent CIF USEC – USGC FOB light crude oil spread

It is not certain that crude pricing will be favorable for Jones Act on average in the future because past relationships aren’t always indicative of future in the energy markets.

For the next decade, if on average, Brent-priced foreign oil is at +2 over the ICE Brent crude futures delivered to the USEC and U.S crude oil in the USGC is averaging between 0 and -3 under the ICE Brent;

Brent USEC +2 Minus JA freight +2.11* USGC -3 ———————————– $2.89/bbl

*The Conservative assumption is: (1 voy/month x $2.11/bbl x 12months x 10 years)/ (1+i)10 = $221,294,233.

While the PV for the 10 years Suezmax charter was $197,428,227 NPV= $23,866,066 in Shareholders’ pockets. There is a world of possibilities to use this Jones Act Tanker.

By chartering a Jones Act Suezmaz, Atlantic Coast refiners, banks and traders can effectively lock the U.S crude oil economics in their favor for the next decade. It’s a gamble on the U.S energy renaissance.

We hope that this article has aroused the curiosity of our readers and will provoke waves because on an Apple-to-Apple basis comparison right now, we can’t prove the myth about Jones Act harming U.S East Coast refiners’ transportation costs.

In the paper we have underscored that timing , not just policies are determining winners and losers in this energy and shipping trade (both international and U.S Flagged).

Oftentimes, a lot of folks talk about trade regulations but at the end it’s always policies within the economics context that drives up all those numbers in the real world.

Finally, we are pointing out the capitalization of a long-term Jones Act charter can yield an even lower transportation cost/bbl that may be used to bet on the crude oil markets conjecture. | ||||||||||||||||||

|

|