RL Blogs

By Simon Jacques

Oct 03, 2016Colonial Pipeline and NYMEX Gasoline price relationships are not immune to changes in historic trends. |

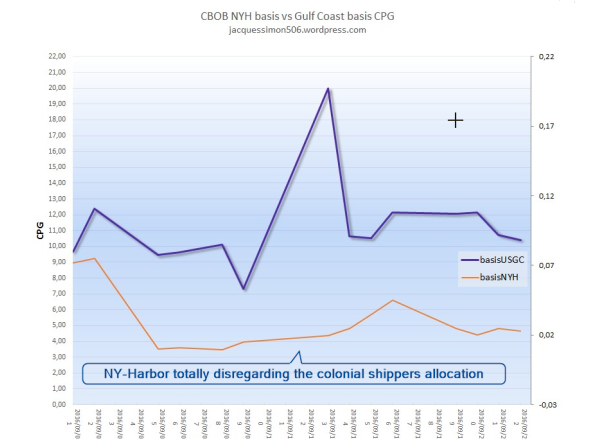

| On September 9 Colonial Pipeline’s Line 1 was halted after a spill in Alabama. As you can see on the graph below, Colonial Pipeline halted on the date marked (1), and the NYH-GC gasoline swap went deeper into inversion.

In Houston, the CBOB basis blew up, not lower as one would expect.

The inversion issue is symptomatic of a much broader shift in the U.S market liquidity. The New York Harbor relative relevance is now reduced to time-spreads, and the culprit is Finance.

In the New York Harbor, inventory storage deals are financed because of the NYMEX EFP connectivity. This banks financing is contingent on the ability to deliver the products on Nymex facilities located in New York Harbor. As a result, European traders are swamping New York Harbor.

It’s not profitable to move gasoline to New York from Houston on its main artery for regular shippers.

The liquidity has shifted to the Gulf Coast.

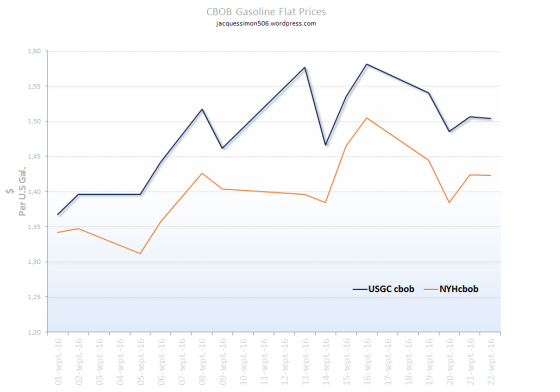

Recently we saw articles opining that non-regular shippers (spot buyers) were “Getting paid to ship products to New York Harbor” because the “line value is negative”.

In this case regular shippers ship (sell products at one point and re-purchase at another) because they have to maintain a minimum volume average shipment history. This pattern has no lower bound and created rigidity at these negative prices.

It is the mindset of the regular shippers to reduce their losses however the buyers are not out there to make a free lunch. With the line “negative price rigidity”, there are still zero incentives to regularly move the products on this flow.

This shows that the relevance of NY harbor and the NYMEX contract aren’t immune from secular industry changes and deep cyclical troughs that materially impact the immediate-term energy markets.

To see more from the Trade, Shipping and Finance Wizard visit: |

|