RL Blogs

By Steve Pagani

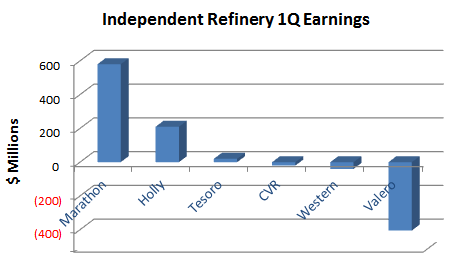

May 20, 2012Independent Refinery earnings in the first quarter 2012 were strong as a result of discounted crude cost and improved operating expenses. Can the independent refinery continue to drive strong results through the rest of the year? |

||||

| For those of us interested in the refinery operations and earnings there is no better place to look than the independent refinery quarterly earnings statements. The independent refinery’s earnings statements can be used to gauge the overall health of the refining industry. Especially because the large integrated companies rarely share as much information concerning crude rates, yields, earnings, and expenses as the independent refinery.

independent refinery capitalized on discounted domestic crude versus foreign or offshore crude oil. The other big factor influencing independent refinery earnings were huge loses in product swap hedging. Many believe that product swap hedging is a great process to lock in margin; however, at times hedging has a very steep cost.

The Winners

Marathon Petroleum had an excellent quarter, out earning all their competitors combined. As independent refineries go they were the top earner in the first quarter. They earned $596 MM in 1Q2012 versus a $529 MM 1Q2011, or a 13% year over

average of $5.65/bbl operating expense. Both also did not suffer excessive hedging losses that might have weighed down overall earnings.

The Unfortunate Ones Valero, Western, and CVR all form an “unfortunate” group of independent refiners that lost a combined $(510) MM due to product hedging swaps. These hedging losses may really be mark-to-market losses so time will tell if they are truly losses, but it is clear that all three are actively using financial instruments to help manage earnings and risk (see Delta Refining).

All three independent refiners also saw increased expenses and decreased production with traditional first quarter maintenance turnarounds. Valero lost $(432) MM in 1Q2012 versus a $104 MM positive 1Q2011, or a 500% decline year over year. Western lost $(53) MM in 1Q2012 versus a $12 MM positive 1Q2011, or a 540% decline year over year. CVR lost $(25) MM in 1Q2012 versus a $45 MM positive 1Q2011, or a 150% decline year over year.

The Conclusion

The story of the independent refinery earnings in the first quarter 2012 was fairly positive with significant discounts on domestic land locked crude. If product hedging results are excluded all companies operated at a significant improvement versus 2011 results.

In an interesting sign of expectations, the independent refiner is utilizing their excess cash not on impressive acquisitions or expansions, but rather on improving their balance sheet and shareholder equity by paying down debt and stock repurchase programs.

| ||||

|

|

.png)

.png)