RL Blogs

By Simon Jacques

May 30, 2016Industrial actions in France demonstrate how modern economies depend on the smooth supply of refinery products. |

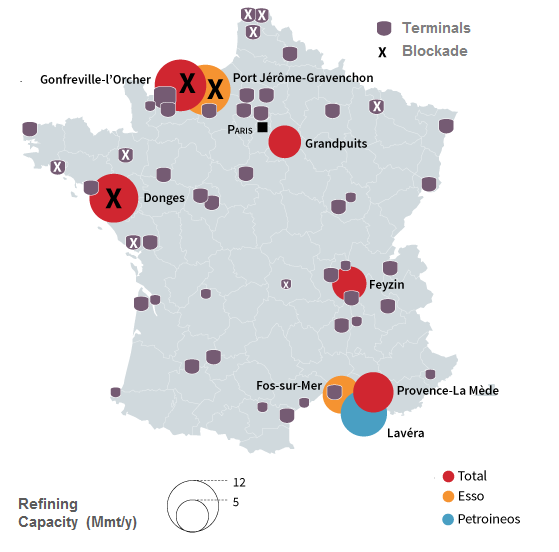

| A blockade at refineries starts to have price and volume effects on a Western Europe nation. Total, the largest refiner in France, has wound down its operations in the hexagon.

Credit: Le Monde

As related by a union representative from "La CGT Total pour un syndicalisme de conquêtes sociales" in Libération "-the goal is to broaden the movement to all businesses in France to a complete blockage of the economy. "

L’Union Française des Industries Pétrolières (UFIP) has estimated that 90% of gasoil stations in the country are supplied normally and has not seen an imminent shortage of fuel.

However scarcity has appeared. Motorists have been lining up to fill up their tanks, fearing that supplies might soon run dry have been told to curtail non-essential fuel purchases at the petrol-stations.

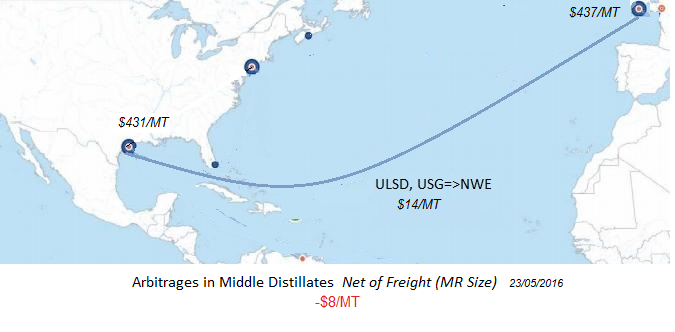

As in a case of other commodities, understanding the paper market, logistics and shipping is key to many successful strategies, which evolve around the arbitrage of location prices (for example the Trans-Atlantic clean products between NWE and the U.S Gulf Coast).

One side of the paper is hedging, the other is speculation...

Speculation plays a noble role in the determination of inventory levels in the physical markets as a strong contango supports the accumulation of inventories by the traders and selling forwards stored commodities.

An influx of financial investors may also cause an increase in the spot prices that is inconsistent with dynamic models of physical flows. Since French strikers have first appeared on May 10th the futures have more than covered the physicals.

The structurally long ULSD speculative position in the U.S Market has not lent support to the steady volumes moving out of the U.S Gulf region.

The NY Harbor market has gone from a negative -35Million barrels net short position at the beginning of 2016 to a 10 Million barrel positive net long position during the month of May.

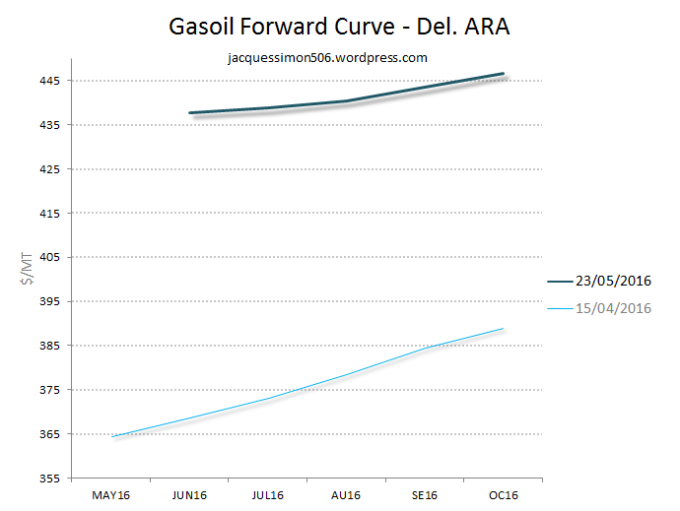

In the European gasoil market, the prompt-contango has narrowed by over 80% from the weeks earlier, limiting the incentive for keeping product in storage. The flattening of the curve and amplitude of the price level is already releasing inventory accumulated during the first months of the year.

A necessary precondition to arbitrage is the ability to arrange at short notice access the products and transportation at the origin and the destination.

When the paper side doesn't synchronize with the physicals, the opportunity doesn't materialize. Freight (in $/MT and premised upon forward-looking estimates for bunker fuel oil, currency and port costs) and the gasoil/diesel prices have made a difficult position for exports movements from U.S Gulf refiners and diesel traders.

The tanker spot business FOB-Houston to Europe (not on the top of existing contracts) should be virtually muted.

The supply disruptions caused by industrial actions in France demonstrate vividly how modern economies depend on the smooth supply of critical liquid fuels but in the recent months, the bias on the paper side has regained its role in the determination of the physical opportunities.

When the paper markets are pushing over a magic threshold, then the economic fundamentals are dragging us to equilibrium: this is the reality that we've actually observed, most obviously over the last months in energies.

To see more from the Trade, Shipping and Finance Wizard visit: |

|

|