RL Blogs

By Simon Jacques

Jan 04, 2015It’s the holiday season but the energy markets never stop. |

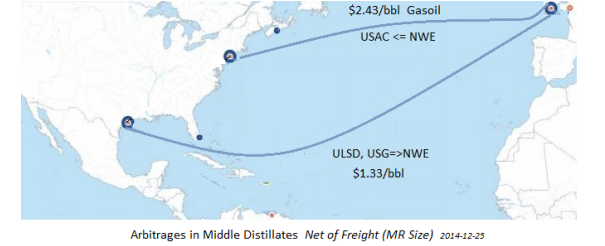

| Ultra-low Sulphur Diesel (ULSD) is trading in the U.S at a premium to values in the U.S Atlantic coast, amid weakness in the ICE high sulfur gasoil futures and below the fair-value tanker clean freight routes.

Several traders are now looking for mid-range vessels to load with ULSD from the U.S. Gulf to Europe and are seeking U.S buyers for European Gasoil.

Traders can now lock a substantial profit per barrel, calculations show and these opportunities could roll into the New Year.

These spreads have widened; a lot of these products are locked into the curve by traders. This week PADD1 diesel-gasoline average was $0.81 per gallon. That’s 23 cents more a gallon compared with a year ago.

The arbitrage window from the USGC is open as well.

Esa Ramasamy, Global Director Strategic Oil Markets Development at Platts, recently stated “As long as refiners can obtain a better margin by exporting ULSD, the pump prices will have to match the export value – otherwise ULSD will flow out of the country and not to the pump.”

U.S Distillate Stocks are in the Lows of the 5-yr Range

One dynamic in the U.S is that refined products are lagging the declining crude oil barrel at the rack during declining markets. My explanation goes like this: wholesalers in PADD1 are able to pass-on the burden of the declining energy prices to their customers at a slower rate than what they pay for their supply.

This ability to exert pricing control creates a premium in the prompt part of the curve, downplaying the expectations from the buy-side at the rack.

Even if the energy prices appear cheap year-to-year, these buyers (gas retailers) make money on thin back-to-back margins) and face margins squeeze.

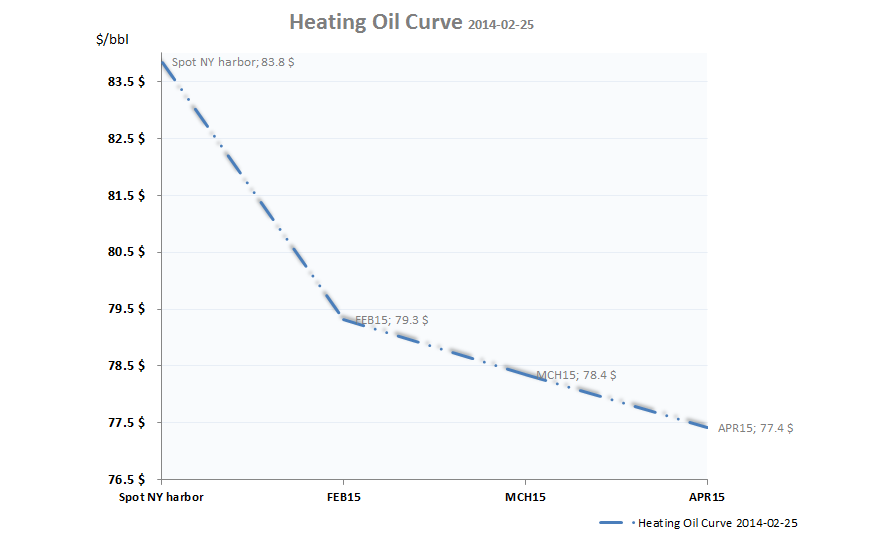

For the buy-side, it is optimal to deferred supply as long as possible. This has led to the backwardation shown below.

European Gasoil is Relatively Depressed to U.S Diesel Markets

Gasoil and Diesel are two middle distillate streams that aren’t perfect substitutes so is not the so-called HOGO spread…

Gasoil is typically a feedstock for crackers and just a nice back-haul for U.S diesel exports. I talk about over 70% of this trade, the rest may be power generation, bunker blending or might be ULSD blending.

For instance, Platts mentioned Vitol’s Russian Cargo bounded to the U.S, it’s likely that they have approached a U.S refiner with a ULSD cargo discounted due to poor tests, the refiner will run it as Gasoil feed straight into the units.

I believe that U.S refiners’ demand for European gasoil demand is mainly sustained by low-natural gas prices in the U.S and the refiners’ quest for better crack margins (currently below 10$/bbl). i.e the price of gasoil gets cheaper for North-American refiners.

To continue this article visit the Trade, Shipping and Finance Wizard at http://jacquessimon506.wordpress.com/ |

|

|