RL Blogs

By Optimization Specialist Robert

May 11, 2014Understanding North American crude rail supply chain economics. |

||||||||||||||

|

While most industry speakers focus discussions on project economics of crude by rail, many do not prepare refiners for managing the logistical realities. The failure to recognize these logistical details can make your crude by rail economics turn from a golden egg to a rotten turd.

The simple truth is that North American crude by rail economics hinge on two main factors – how wide the WTI vs Brent arb remains, and how long it will remain materially disconnected. Deviations from project assumptions on these two factors can derail a promising dream.

While I do not believe that many refiners will lose money on their rail investments, I know that many will be surprised that they are not making as much as they expected. Not including the capital invested, crude by rail operations will typically cost between $10 - $15 per barrel of crude transported. Listed below are operational factors that need to be considered in determining the economic viability of receiving crude by rail.

Rail Car Size Rail cars come in many sizes, and rail cars that transport crude (i.e. tanker cars) typically vary between 25,500 – 31,800 gallons. This is roughly 600 – 750 barrels per tanker car for those that speak refinery.

Since rail cars are in such a high demand, many rail leasing or construction companies do not differentiate size and offer similar rates for different sized cars. While this will not significantly affect the rail opex, this can sizeable affect gross margin with lower discounted crude receipts.

Cycle Time The cycle time of a refinery rail fleet is the single most important metric that one should monitor. Refiners with the lowest fleet cycle time will have the most significant advantage for rail economics. Low cycle times enable minimization of rail fleet size or maximization of railed crude throughput.

Let’s take the example of a US Gulf Coast refiner seeking to rail crude from Bakken on a 500 car railfleet, with each railcar having a capacity of 750 bbls. If this rail fleet has a cycle time of 30 days (makes a round-trip journey once per month), this refinery can receive roughly 12,500 bbls of crude a day by railcar.

If this refinery can reduce the cycle time by 5 days from 30 to 25 (roughly 16%), then the two following options can be considered: rail fleet can be reduced by 84 cars to achieve the same throughput, or throughput can increase from 12,500 bbls/day to 15,000 bbls /day. While the applicable option will depend on refinery capabilities, both scenarios have large benefits.

Unit Trains vs Manifest Cars Unit trains are a group of rail cars (typically between 40 - 120 railcars) that move as a solid train from one location directly to another. Naturally, this is the most efficient mode of operation from a logistical and cycle time perspective. By contrast, manifest cars are individual cars or small groups of cars, and need to wait for additional cars to collect together before being shipped to a destination.

When refineries consider crude by rail projects, Unit Train capability is a top priority. Not only does a refiner achieve economies of scale for project design, but cycle time efficiency is the highest with unit trains. Refineries can still have economically viable projects with manifest car designs; however, at the expense of higher operating costs or lower throughputs. Not only will cycle times increase with manifest car operations, but demurrage and non-ratable receipts will occur as cars bunch and get delayed.

Lease Term and Lease Fee Here is your chance to gamble again when deciding your rail fleet accumulation strategy.

Do you buy? Do you lease? If you lease, how long, and for what rate?

All of these are very important questions to consider. Between buying or leasing, this likely depends on the size and type of company that operates a refinery. The following are scenarios that likely hold true:

If your refinery finds itself in the position of having to lease railcars, the decision then becomes a trade-off between lease term and lease rate. In today’s market, short term rail leases (< 1 yr) can fetch $2000 per car per month (PCPM). For a 500 railcar fleet, this equates to a rail lease cost of $1 Million a month!

In comparison, long term rail leases of say 5 years or greater, can carry a lease rate of $1000 PCPM. While longer rates can significantly reduce lease fees by at least a half, they carry a longer term obligation. So the real question becomes how long do you believe this mid-continent crude discount to remain large enough to warrant crude by rail operations?

“the real question becomes how long do you believe this mid-continent crude discount to remain”

The reality is that many industry analysts anticipate the WTI-Brent arb to narrow substantially over the next couple of years due to improving crude pipeline infrastructure. As this occurs, the rail bubble will collapse, and the market for over-supplied railcars will start to deepen. At this point, those with shorter term rail leases will be able to pick up railcars cheaply.

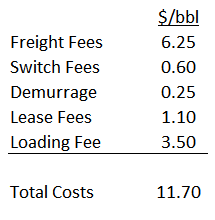

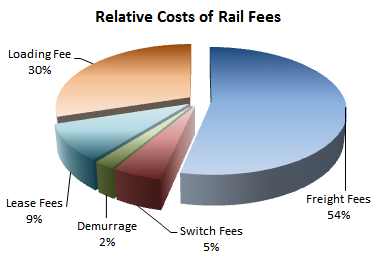

At the end of the day, lease fees are not the largest contributing factor to crude by rail operating expenses. They range between $0.5 - $3.0 /bbl depending on the factors discussed above.

Railway Fees So far I’ve only discussed the costs related to railcars alone, but let’s not forget that the backbone of this entire operation is the railway itself. Rail companies charge fees to use their railways, and these charges add up.

Just to list a handful of charges, one can expect to see: Freight Fees, Switch Fees, Storage Fees, Handling Fees, and Diversion Fees among others. Note in the image below depicting the numerous amounts of rail companies within the U.S. Depending on the distance that the crude railcars travels, and the number of railway companies involved, railway fees can vary between $5 - $12 /bbl.

Loading Fees Crude delivered by rail begins life in a pipeline, so special handling is required to load it into a railcar. Whether crude can be loaded directly into a railcar from a pipeline, or requires transloading from a pipeline to a truck, then to a railcar, these operations carry a fee. Depending on the number of transfers required, and the distance between each mode of transfer, these fees can range between $1 - $4 /bbl.

All in all, crude by rail is a very complex business opportunity. Beyond the $20 - $60 Million dollars of infrastructure investment required to enable crude railcar receipts, there are additional routine operating costs that add up quite substantially.

This appears to be an easy decision to make when the WTI-Brent differentials are as wide as $20/bbl, but let’s give careful thought to how long you expect this spread to remain. It will only be a matter of time until we see who the real winners and losers are.

|

.png)